📝 Market Commentary for 2023-Q1

This quarter, we witness the rise of BRICs, potential political pushback to Fed policies, a new BOJ governor, and the looming development of a credit crunch and recession.

We conduct in-depth investment research and provide commentary on the most significant market events of the previous quarter and provide an outlook for the current investing environment.

Do not reply to this email with any service requests, contact us for support if needed.

Q1 2023: A Continued Rebound for Risk Assets.

During the first quarter of 2023, the equity market continued to bounce back, with technology and consumer discretionary stocks leading the way. However, the broader market and small-cap stocks did not participate as strongly. On the other hand, bonds and investment-grade credit saw modest gains as people worried about a deflationary event caused by bank failures. Commodities ended the quarter with noticeable losses due to recession concerns as well, while the US Dollar index remained mostly unchanged.

BRICS Challenge the Western-Led Hegemony.

The geopolitical landscape has been undergoing significant shifts as emerging powers challenge the established order dominated by the United States and its Western allies. One of the most significant developments in this regard has been the formation of the BRICS (Brazil, Russia, India, China, and South Africa) as a new power bloc. The BRICS countries collectively represent a significant share of the world's population, resources, and economic potential, and are increasingly asserting themselves on the global stage.

As part of this shift, Saudi Arabia and Brazil, two countries that have traditionally been close U.S. allies, have begun to tilt towards China. This is driven in part by economic considerations, as China is now the largest trading partner for both countries. In the case of Saudi Arabia, this has led to a strategic partnership between the two countries, with China investing heavily in Saudi infrastructure and energy projects. Similarly, Brazil has sought to deepen ties with China, particularly in the agricultural sector, where it hopes to increase exports to China.

These developments have significant implications for the balance of power in the world. While the United States remains the world's preeminent superpower, the rise of the BRICS and the shifting alliances of key players like Saudi Arabia and Brazil suggest that the geopolitical landscape is becoming increasingly complex and multipolar. As such, it is likely that we will see a more diverse range of power centers emerge in the coming years, with China playing an increasingly prominent role.

Political Pushback Starting Against Fed Policies.

In the United States, the Federal Reserve continues to tighten monetary policy, raising interest rates by 25 bps in March, and continuing “quantitative tightening.” These policies are starting to be met with criticism from the general public and policymakers. Luigi Zingales, a professor at the University of Chicago, is calling for an independent commission to investigate the Federal Reserve's handling of inflation and the banking crisis. He believes that the Fed has failed to see both coming and that the banking system cannot function with rates of 4% or higher. Zingales suggests that the Fed needs to soften interest rates and find ways to soften the banking crisis, especially for small and medium-sized businesses. He also emphasizes the importance of regional banks in lending to small businesses and minorities.

The Federal Reserve has implemented economic policies that could put pressure on President Biden's administration. Powell and other Fed officials have signaled that the Fed may continue to raise interest rates and hold them at elevated levels, which could slow down economic growth and potentially harm employment figures for the United States, causing political challenges for Democrats. Last quarter, we talked about Triffen’s Dilemma, which is a conflict of interests that arises between short-term domestic and long-term international objectives for countries whose currencies serve as the global reserve currency. This theory predicts that the United States will eventually sacrifice the dollar for the stability of its domestic markets.

Bank of Japan Sees Governor Change.

The leadership change at the Bank of Japan is a historic event coming at a consequential time for global markets across asset classes. Governor Kuroda's unprecedented decade-long tenure of non-stop radical easing and policy experimentation may be coming to an end, and the keys of the world's duration anchor will be handed over to incoming Governor Ueda. This change will result in the weight of the global bond markets and rates markets, as the bank will undergo the most important leadership change in the modern era of modern central banking.

We have repeatedly highlighted the unusual situation of the Bank of Japan, as it is the final major central bank that is still engaging in quantitative easing. A change in policy to allow for higher interest rates may influence global assets, as a financially restrictive central bank has effectively pushed most Japanese investments abroad. If the BOJ expands its yield curve control range, domestic assets may become appealing enough to prompt the sale of foreign assets held by Japanese capital and their subsequent repatriation. Nevertheless, the BOJ should exercise caution when reducing its supportive policies, as increased debt servicing costs could lead to fiscal consequences.

Credit Crunch and Recession Loom in the U.S.

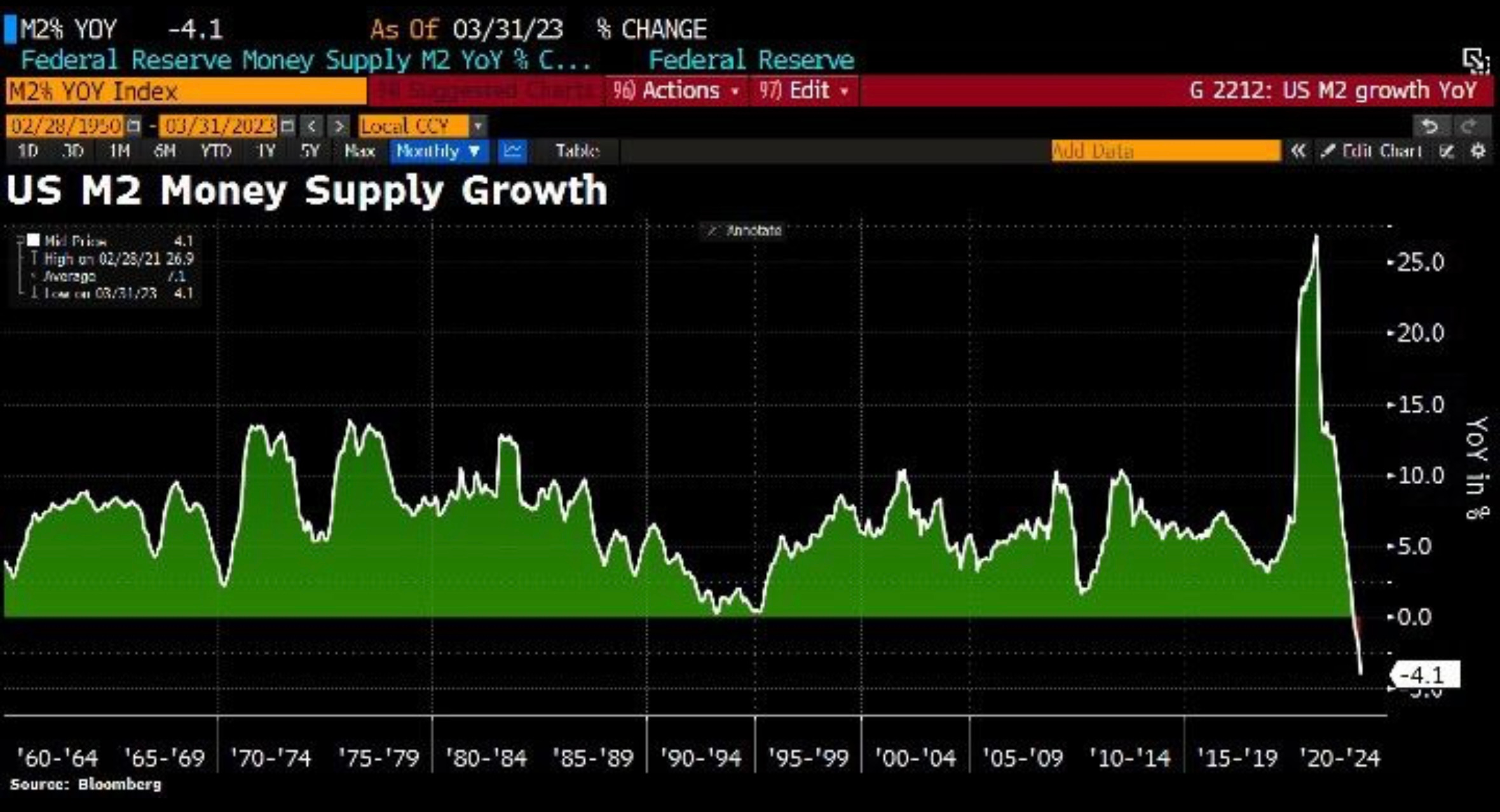

Two major banks, previously seen as safe depositories, have failed, leading to tighter lending standards and increased credit crunch risk. The SVB First Republic banking crisis could lead to a credit event and a deflationary spiral in the economy. A credit event occurs when confidence in the financial system is shaken, causing investors to demand higher interest rates for loans and credit or become reluctant to lend money altogether. This results in a decrease in the money supply, leading to a deflationary spiral. In this scenario, the decline in lending and borrowing activities, coupled with lower consumer spending, can cause a drop in risk asset prices and economic activity. We have already seen signs of this occurring, with M2 Money Supply Growth reaching historically negative territory.

However, U.S. stocks have remain ebullient throughout the quarter, possibly due to some clients' belief that the Fed/FDIC bailout of depositors is a form of quantitative easing. The money supply is likely to continue falling sharply with these bank failures. It is of note that stocks and bonds now are exhibiting a more traditional, negative correlation, with stocks going down when rates fall and vice versa. The equity risk premium (ERP) remains subdued, however, making risk/reward in U.S. equities unattractive, in our opinion.

Current Outlook and Positioning

Although the market has rallied this quarter, we remain less constructive on risk assets such as equities, and more constructive on assets that pay a fixed rate, such as short duration fixed income. We believe that deflation is now the more likely risk, although we believe there to be volatility within the inflation figures. Investment grade credit remains more attractive than high yield debt, as we anticipate credit spreads to widen in the event of a credit crunch.

The U.S. Dollar continues to remain weaken, so non-U.S. assets look attractive. While we like emerging market equities as a whole, we prefer picking country by country, as geopolitical risks remain elevated. From an economic sector standpoint, we have become more defensive, favoring non-cyclical stocks and those with less leverage and solid balance sheets. We also continue to hold an allocation to precious metals, within each strategy's risk parameters.

Written by Joseph Lu, CFA®

Joseph is the founder and a managing director of Conscious Capital Advisors, as well as a CFA® Charterholder.

🔗 Connect with us on LinkedIn, Facebook, or Twitter.

Have a question about what we shared? Email us at info@consciouscapital.pro.

Do not reply to this email with any service requests, contact us for support if needed.

The information presented in this newsletter is for educational purposes only and is not a solicitation or recommendation for any specific security, product, service, or investment strategy.

Investments involve risk and unless otherwise stated, are not guaranteed. Be sure to consult with a qualified financial advisor, tax professional, or attorney before implementing any strategy or recommendation you may read here.